Why Waiting To Buy or Sell Is

More Costly Than You Think!

.

For those buyers that have been holding back, waiting for the market to drop or interest rates to level off before making a decision - your ‘waiting game’ has cost you money.

For sellers trying to time the "peak of the market" you have missed that opportunity. That train has already left the station. The market has shifted to stabilize that runaway train we have experienced the last 1.5 years.

Everything has a "cost," and in Economics 101 cost of waiting would be defined as an “Opportunity Cost” or 'the missed benefit that would have been derived from an option not chosen,' buying or selling versus waiting.

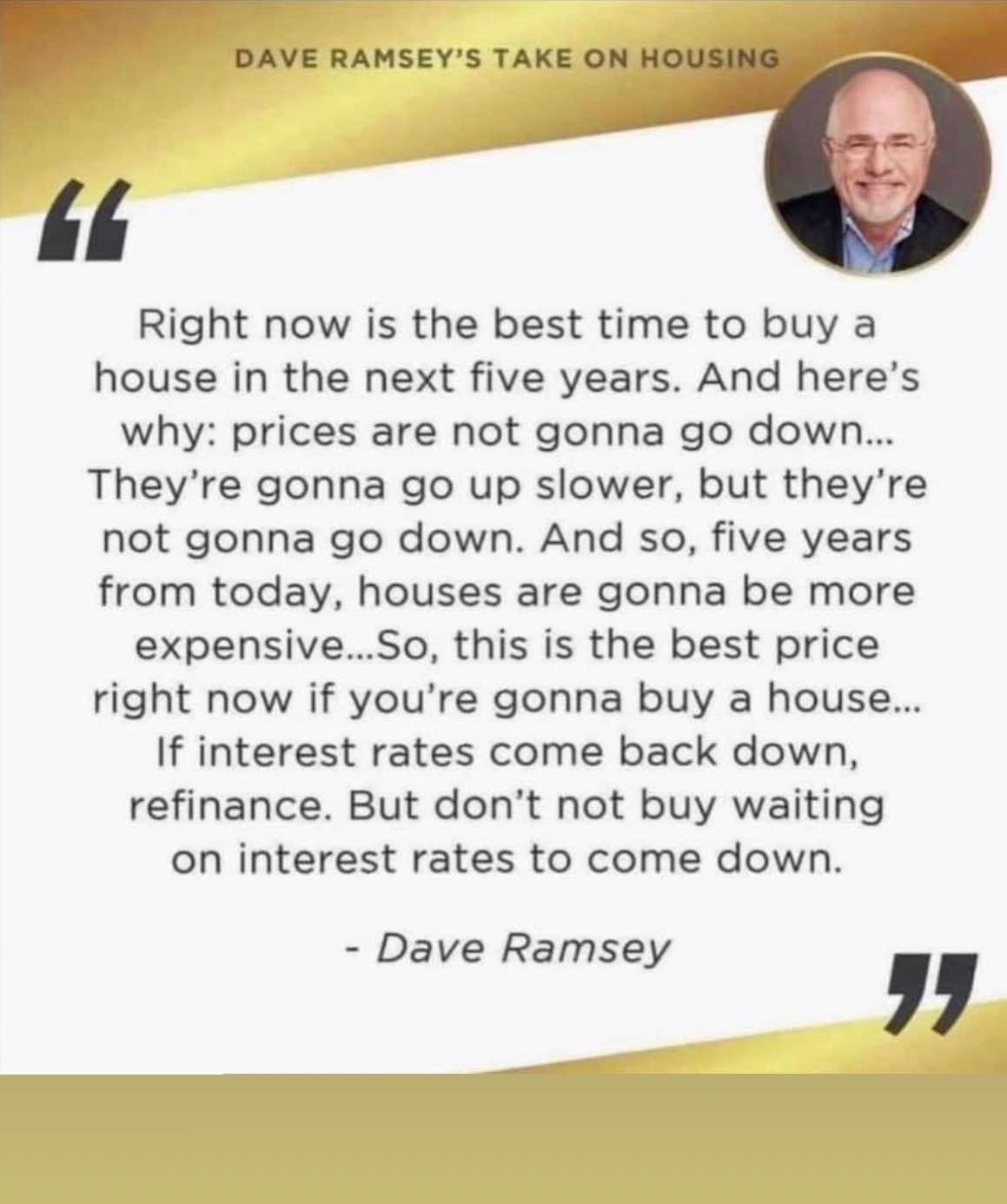

As you'll see, the following are additional reasons supporting Dave Ramsey's (well known finance guru) comment that this is one of the very best times to sell or buy a home. There are two basic questions you should be asking regardless of whether you are a buyer or a seller:

What is likely to happen to home prices in the coming year? Although the outrageous prices we’ve experienced this last year have begun leveling off slightly, prices will continue to go up based on the number of people relocating to our area.

Where will mortgage rates be by the end of this year? Next year? Very important questions unless you're buying with cash!

What is likely to happen to home prices in the coming year? Although the outrageous prices we’ve experienced this last year have begun leveling off slightly, prices will continue to go up based on the number of people relocating to our area.

Where will mortgage rates be by the end of this year? Next year? Very important questions unless you're buying with cash!

The consensus is that mortgage rates will continue to rise steadily increasing over the next three years. According to a report released by the New York Federal Reserve rates are expected to reach 6.7% by 2023 and 8.2% by 2025.

Now, let's check the local Dallas-Fort Worth Metroplex (DFW) outlook. According to the Texas Real Estate Research Center at Texas A&M, the forecast is for home prices to slack off a bit from this past years double-digit growth but still be in the 9% to 10% annual appreciation range. This will be due to the continued hot job market in our area bringing an influx of new residents coupled with a continued tight housing supply.

As home prices in the DFW metroplex continue to rise well above the national average, let's look at a home valued today at $450,000 with a 9% annual appreciation. At the end of the year, in just 6 months, this home would be valued at $470,250 or an increase of $20,250 above the purchase price.

This begs the question: can you really afford to wait and lose over $20,000 in potential equity or worse find yourself priced out of the home you want?

The other basic question to be answered is mortgage rates - what will happen to them in a growing inflationary market?

Where are mortgage rates expected to be by the end of this year?

The interest rate on a conventional, 30-year fixed rate mortgage has risen continually since January as the Federal Reserve has raised interest rates in an effort to quell inflation. According to Bankrate® the current rate for a 30-year fixed rate mortgage in the DFW metroplex is 5.61% depending on credit score and other lender qualification factors such as Debt To Income (DTI) and the Loan-To-Value (LTV).

Increase the mortgage interest rate and your monthly payment, Private Mortgage Insurance or PMI, all increase as well as how much you will have paid at the end of the loan.

What do rising home prices and mortgage interest rates mean?

Very simply, it means that you will pay more for the home you want, if you can still afford it, because in some cases you may not be able to meet the lender qualifications if you wait.

Let’s assume you purchase a $450,000 home now with a current 5.71%, 30-year fixed-rate loan. After making a 20% down payment your monthly mortgage payment (principle and interest only) will be $2,092.

It should be obvious that waiting until the end of the year for the same or comparable home in the DFW metroplex is projected to cost $470,250 and a 30-year fixed-rate conventional mortgage could be hovering at or above 6% based on the industry forecasts above. This brings the new monthly mortgage payment (principle and interest only) to $2,256 - a difference in the  monthly mortgage payment of about $164. Yet, there are more escalations to be considered such as home insurance, that is also based on the valuation of the home, so $164 increase is just a start, assuming you still qualify! Remember, this is only in 6 months!

monthly mortgage payment of about $164. Yet, there are more escalations to be considered such as home insurance, that is also based on the valuation of the home, so $164 increase is just a start, assuming you still qualify! Remember, this is only in 6 months!

One of the basic mortgage qualification criteria is a Mortgage-To-Income ratio of 28%. This means the mortgage payment cannot be greater than 28% of your gross income. Although this varies among lenders, this is a relatively safe benchmark. To still qualify for a comparable home at $470,250 you would need to show the lender approximately $7,028 in additional annual gross household income at the end of 2022 versus buying it now in mid-2022!

Bottom Line

When considering the purchase of a home, you are likely motivated by some of the non-financial benefits, such as security, stability, privacy and control over your living space.

However, it is the financial benefits that can make it clear that doing so today is much more advantageous than waiting for six months to a year. Remember the old adage, "nothing gets cheaper with time."

If you’re interested in buying a home, we have a list of ‘Off Market” homes that are not in MLS. Call 469-556-1185.

One question we're frequently asked is 'with such a "hot" market how can I sell when I can't make an offer on a home until mine is sold. Either way I am taking a big risk!'

We have several solutions for you to consider that can allow you to move out of your current home and into your new home with relative ease and no risk. Just check the appropriate box below and we can get with you and answer your questions.

Please put a link to our blog site in your internet browser bar so you can check back on our blogs as they are published every week.

To Paint or Not To Paint, That is The Question